Essential Documents Needed for Property Loans in Dubai

Published :

Last Updated :

Published :

Last Updated :

Real estate investors and homebuyers actively choose property loans as their preferred financing method within the Dubai market. People from residence categories can follow a simple path to obtain mortgages provided they prepare all necessary documentation. Banks and financial institutions based in Dubai enforce strict procedures that check how suitable candidates are for loans by evaluating their financial standing and ability to repay funds. Loans risk rejection, and delays appear when an applicant presents flawed or insufficient documentation to the financial institution.

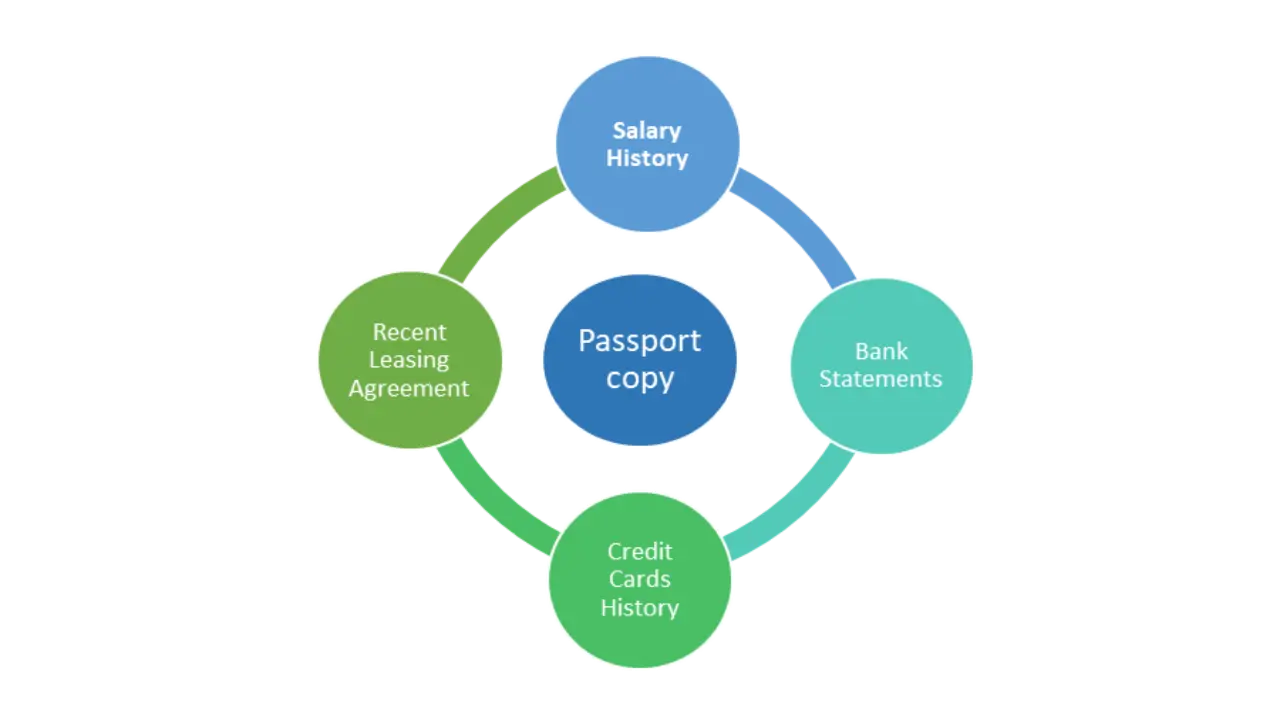

Knowledge about the essential documents before an application helps reduce time during the approval phase. All applicants must supply basic documentation that includes their passport, Emirates ID, or bank statements, while additional materials, including salary proof, business permits, and financial records, depend on personal conditions. This blog shows you what you need to apply to get property financing in Dubai so you can start your loan process with a bank or lender. When everything is properly organized you will enhance your opportunity to secure a loan both fast and with desirable conditions.

Your income, employment status and residency are some of the factors that determine whether you can secure a loan for your home in Dubai. UAE nationals and expatriates can both apply for mortgages, but the eligibility criteria vary slightly.

Mortgage conditions are more favorable for Emirati citizens. Most banks disburse 80%-85% value of property as a loan depending on income and type of property. To qualify, applicants must:

Even expatriates have access to home loans, but the terms are a little stricter. Financing of 80% is common for them. Eligibility includes:

Both nationals and expats need to be creditworthy as determined by the bank and be in a position to repay the loan comfortably.

Documents Required for Property Loan Based on Employment Status Here is a breakdown of the UAE Nationals by Salaried and Self-Employed.

Are you looking to purchase a house in Dubai with bank financing? Here’s the step-by-step guide to securing a mortgage to help cover your home purchase.

The initial step to obtaining a mortgage in Dubai is to determine which lender to use. Mortgages come in different forms through different banks and financial institutions, so you have to compare the interest rates, loan terms, and eligibility criteria. Some banks will have specific policies for residents and non-residents, so be sure to check their policies before applying.

You can go directly to banks or go through a mortgage broker who can source the best deal for you. Brokers have access to several lenders and will be able to get you a better rate. The right lender will set you up for a smooth process and great financing options on the property you would like to purchase.

There are fixed-rate, variable-rate & Islamic home finance available in Dubai. Fixed-rate mortgages offer stability with constant payments, while variable-rate loans can fluctuate depending on market conditions. Islamic home finances are structured according to Sharia principles such as Murabaha or Ijarah.

Before doing so, note factors such as the term of the loan, down payment requirements, and interest rates. Down payment requirements may be higher for expats and non-residents than for UAE nationals. Consider your options carefully to choose a mortgage that suits you financially and in the long run.

A mortgage pre-approval letter is a document that is provided by the bank to confirm how much loan you qualify to take out based on your income and financial health. It allows you to establish a practical budget before you begin looking for a home.

Thereafter, the bank will assess your proof of income, credit score, and current outstanding liabilities before granting you pre-approval, which is typically valid for 60–90 days. Having this letter makes you a more competitive buyer, and your position for negotiation with sellers has been improved. It also accelerates the loan approval process once you settle on a property.

Now that you’ve been pre-approved begin searching for a property that aligns with your financial and personal wants. Partner with real estate agents, explore online listings and visit properties to identify the perfect home. Make sure your chosen lender is approved for the property you choose since banks will often have restrictions against certain developments.

When you have located the desired property, you should sign a Memorandum of Understanding (MoU) with the seller as well as pay a deposit (usually 10%). A MoU will quote the terms of the sale, which is one of the most critical elements of the process of applying for the final mortgage.

Once the MoU is signed, the bank will carry out a property valuation to cross-check its market value before lending approval. Upon approval, you sign a loan agreement and place your down payment. Your bank will issue a mortgage cheque to the seller, and the ownership is transferred to the Dubai Land Department (DLD). Also, alongside that, you will need to pay DLD Fees, Mortgage Registration Fees, and Agent Commission. After this process is complete, you are granted the title deed that gives you status as the official owner of that property.

While applying for a mortgage in Dubai, it is essential to know the major terms and conditions of your loan that would influence your mortgage repayment and overall financial commitment. There are several key things to keep in mind.

In Dubai, the mortgage interest rate could be fixed or variable. A fixed-rate mortgage locks in the interest rate for a certain period, creating stability in monthly payments. A variable-rate mortgage will change according to the market, which can see your repayments reduce or increase over time.

The loan tenure is the duration over which you repay your mortgage. Most mortgages in Dubai are 15 to 25 years long, with some banks offering terms of up to 30 years for UAE nationals. A longer tenure results in lower monthly payments and higher interest paid, while a shorter tenure increases monthly payments and lowers the total interest paid.

Banks may charge an early settlement fee for you to pay off your mortgage early. This is typically 1% to 3% of the outstanding loan amount. Some banks have a grace period before this fee is applied, and with some, there are zero chances to avoid the fee. Make sure to verify this condition before you sign your loan agreement.

Loan-to-Value (LTV) ratio helps them decide what percentage of the property value is financed by the bank. UAE Nationals enjoy an LTV of up to 85%, whereas expats generally qualify with up to 80% LTV. Non-residents can have a lower LTV, approximately 50-60%, etc. The more you put down, the less you have to borrow, which means the lower your payments and the better your interest rates.

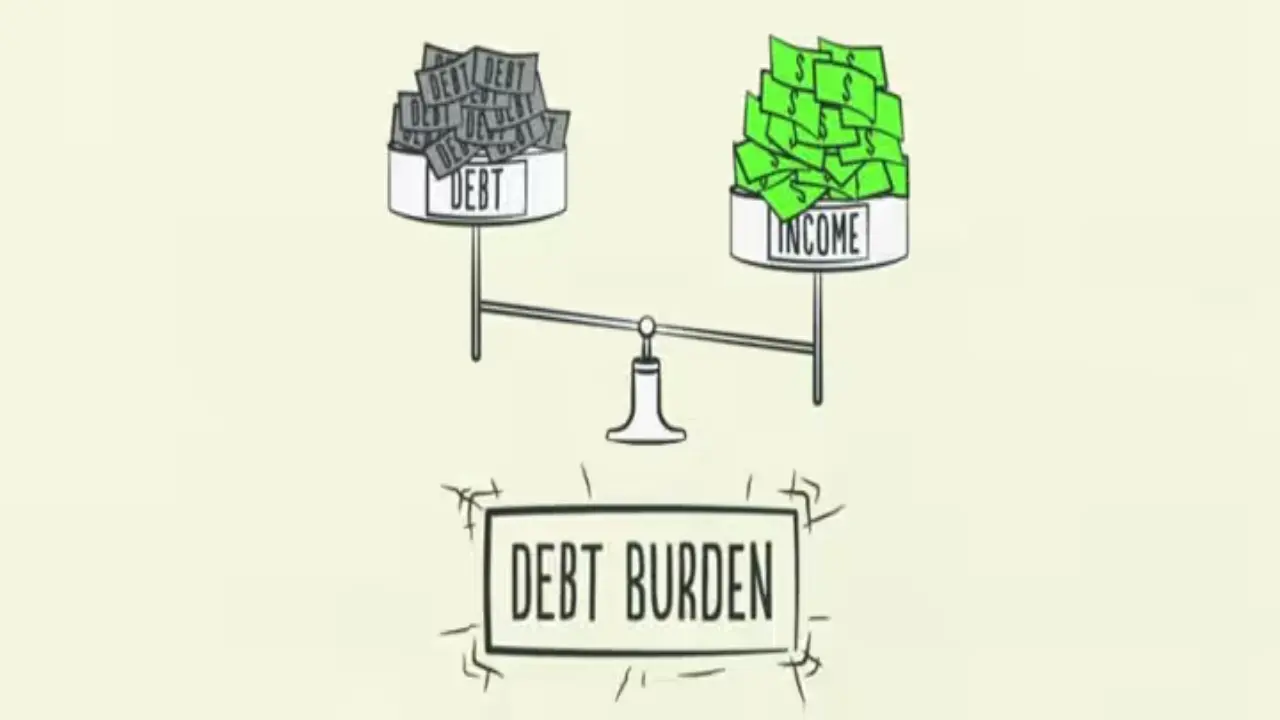

One of the primary factors affecting their eligibility for mortgage approval is the Debt Burden Ratio (DBR). According to the UAE Central Bank, no more than 50% of an individual’s monthly income may be allocated toward total monthly loan repayments — including credit cards and personal loans. If your DBR is too high, your mortgage application may get rejected, or you may be eligible for a lower loan amount.

Planning well, understanding eligibility criteria, and preparing the necessary documents are all part of obtaining a property loan in Dubai. Regardless of whether you are a UAE national, expat or non-resident, fulfilling the bank’s conditions and sustaining a good financial profile can enhance the odds of getting your mortgage approved. The choice of lender and the type of mortgage (fixed or variable) will affect your long-term financial obligations, while other factors such as loan tenure, LTV ratio, and DBR will help you decide on the amount that can be borrowed.

You should also be aware of added costs, such as early repayment penalties, DLD fees, and valuation charges. A mortgage pre-approval helps you know your budget and strengthens your position as a buyer. Mortgage brokers or Financial Advisors can also make the process easier for you and help you get the best deal.

Armed with know-how on terms and preparation, you can make an informed decision for property investment in Dubai. Whether you're purchasing a house for personal use or as an investment, having your finances in order will facilitate the transaction process and provide secure prospects for the future in the thriving UAE’s real estate sector.

While getting a mortgage pre-approval usually takes around 3-7 days, the final approval process post-property selection ranges from 2 to 4 weeks, depending on the lender’s process and document verification.

No. But in Dubai, the interest rate is relatively low compared to other cities. Although the interest rate varies from bank to bank, foreigners typically receive a Dubai mortgage at an interest rate of 3% to 5%.

In Dubai you can look for a 25-year mortgage. In general, mortgage terms in Dubai are between 5 and 25 years. Note that the maximum loan tenure varies depending upon the age and other factors of the borrower.

In addition to the payment, you need to pay following:

1) The buyer also pays DLD fees (4% of property value) 2) Mortgage registration fees (DLD) 3) Bank processing fees 4) Property valuation charges 5) Agent commissions for the purchase.Yes, a few banks provide loans for off-plan properties, but their LTV ratios are lower, and finance is subject to developer approval. Banks usually finance up to half of off-plan purchases.

Your gateway to offline planning in the digital realm. Discover a world of real estate opportunities through our immersive offline property website experience

Apartments

Townhouses

AED 1,250,000

Emaar South

1, 2 & 3

719 - 2603 Sq Ft

Apartments

Villas

AED Price on Request

Dubailand

Apartments

AED Price on Request

City of Arabia

Apartments

AED 560,000

Dubai International City

Studio, 1 & 2

385 - 1362 Sq Ft

Commercial

AED Price on Request

Motor City

Apartments

Studios

AED 599,000

Dubai South

Studio, 1 & 2

Apartments

Townhouses

AED 1,250,000

Emaar South

1, 2 & 3

719 - 2603 Sq Ft

Apartments

AED 1,600,000

Dubai Islands

1, 2 & 3

582 - 3256 Sq Ft

Apartments

Villas

AED Price on Request

Dubailand

Apartments

AED Price on Request

Meydan

Apartments

AED Price on Request

City of Arabia

Apartments

AED 560,000

Dubai International City

Studio, 1 & 2

385 - 1362 Sq Ft

Commercial

AED Price on Request

Motor City

Commercial

AED Price on Request

Damac Lagoons

Apartments

Commercial

Penthouses

AED 2,000,000

Meydan

1, 2 & 3

640 - 4244

Apartments

Commercial

AED 1,900,000

Sheikh Zayed Road

1, 2 & 3

Apartments

Commercial

AED 1,142,000

Damac hills

1 & 2

740 - 6588 Sq Ft

Commercial

AED Price on Request

Mohammed bin Rashid City

Apartments

Duplexes

AED 1,670,000

Dubai Islands

1, 2 & 3

848 - 2607 Sq Ft

Apartments

Duplexes

AED 679,000

Jumeirah Village Circle

Studio, 1 & 2

388 - 2159 Sq Ft

Apartments

Duplexes

AED 2,661,000

Dubai Islands

1, 2, 3, 4 & 4

60 - 9121 Sq Ft

Apartments

Penthouses

Duplexes

AED 9,000,000

Business Bay

2, 3, 4 & 5

2154 - 22900 Sq Ft

Apartments

Studios

Duplexes

AED 830,000

Dubailand

Studio, 1, 2 & 3

420 - 3800 Sq Ft

Apartments

Penthouses

Duplexes

AED 2,390,000

Dubai Islands

1, 2, 3 & 4

757 - 5826 Sq Ft

Apartments

Penthouses

Mansions

AED Price on Request

Palm Jumeirah

1, 2, 3, 4, 5 & 6

1541 - 12382 Sq Ft

Villas

Mansions

AED 20,000,000

Mohammed bin Rashid City

5 & 6

13,007 - 13,568 Sq Ft

Apartments

Penthouses

Mansions

AED 5,500,000

Palm Jumeirah

1, 2, 3, 4, 5 & 6

940 - 11830 Sq Ft

Mansions

AED 65,000,000

Jumeirah

7

41550 - 49062 Sq Ft

Mansions

AED Price on Request

Tilal Al Ghaf

6 & 7

Mansions

AED Price on Request

Damac Islands

Apartments

Penthouses

AED 3,900,000

Dubai Islands

2, 3 & 4

1017 - 7008 Sq Ft

Apartments

Penthouses

AED Price on Request

Jumeirah Garden City

Studio, 1 & 2

1026 - 2255 Sq Ft

Apartments

Penthouses

Duplexes

AED 9,000,000

Business Bay

2, 3, 4 & 5

2154 - 22900 Sq Ft

Apartments

Penthouses

Duplexes

AED 2,390,000

Dubai Islands

1, 2, 3 & 4

757 - 5826 Sq Ft

Apartments

Penthouses

AED 26,000,000

Business Bay

3, 4 & 5

6684 - 43059 Sq Ft

Apartments

Penthouses

AED Price on Request

Rashid Yachts and Marina

1, 2, 3, 4

729 - 2974 Sq Ft

Apartments

Studios

AED 599,000

Dubai South

Studio, 1 & 2

Apartments

Studios

AED 650,000

Dubai Land Residence Complex

Studio, 1 & 2

420 - 1600 Sq Ft

Apartments

Studios

AED Price on Request

Dubai Investments Park

Studio, 1 & 2

390 - 2421 Sq Ft

Apartments

Studios

AED 666,000

Sheikh Zayed Road

Studio, 1, 2 & 3

Apartments

Studios

AED 670,000

Jumeirah Village Circle

Studio, 1 & 2

420 - 1350 Sq Ft

Apartments

Studios

AED 595,000

Dubai Land Residence Complex

Studio, 1 & 2

371 - 1450 Sq Ft

Apartments

Townhouses

AED 1,250,000

Emaar South

1, 2 & 3

719 - 2603 Sq Ft

Townhouses

AED Price on Request

Dubai Investments Park

2, 3 & 4

Townhouses

AED Price on Request

Dubai South

Townhouses

AED Price on Request

Dubai South

Townhouses

AED 4,750,000

Dubai South

4 & 5

3801 - 4915 Sq Ft

Apartments

Townhouses

AED Price on Request

Emaar South

1, 2 & 3

791 - 2778 Sq Ft

Apartments

Villas

AED Price on Request

Dubailand

Villas

AED Price on Request

Mohammed bin Rashid City

5 & 6

Villas

AED 4,900,000

Jebel Ali

4 & 5

2966 - 8231 Sq Ft

Villas

AED Price on Request

The Heights Country Club & Wellness

Villas

AED Price on Request

The Heights Country Club & Wellness

Villas

AED 4,000,000

Sobha Sanctuary

4 & 5

2459 - 3430 Sq Ft

Subscribe to our Daily, Weekly and Monthly Newsletters, Expert Advice and Latest Launch with Zero Spam, Unsubscribe Anytime.